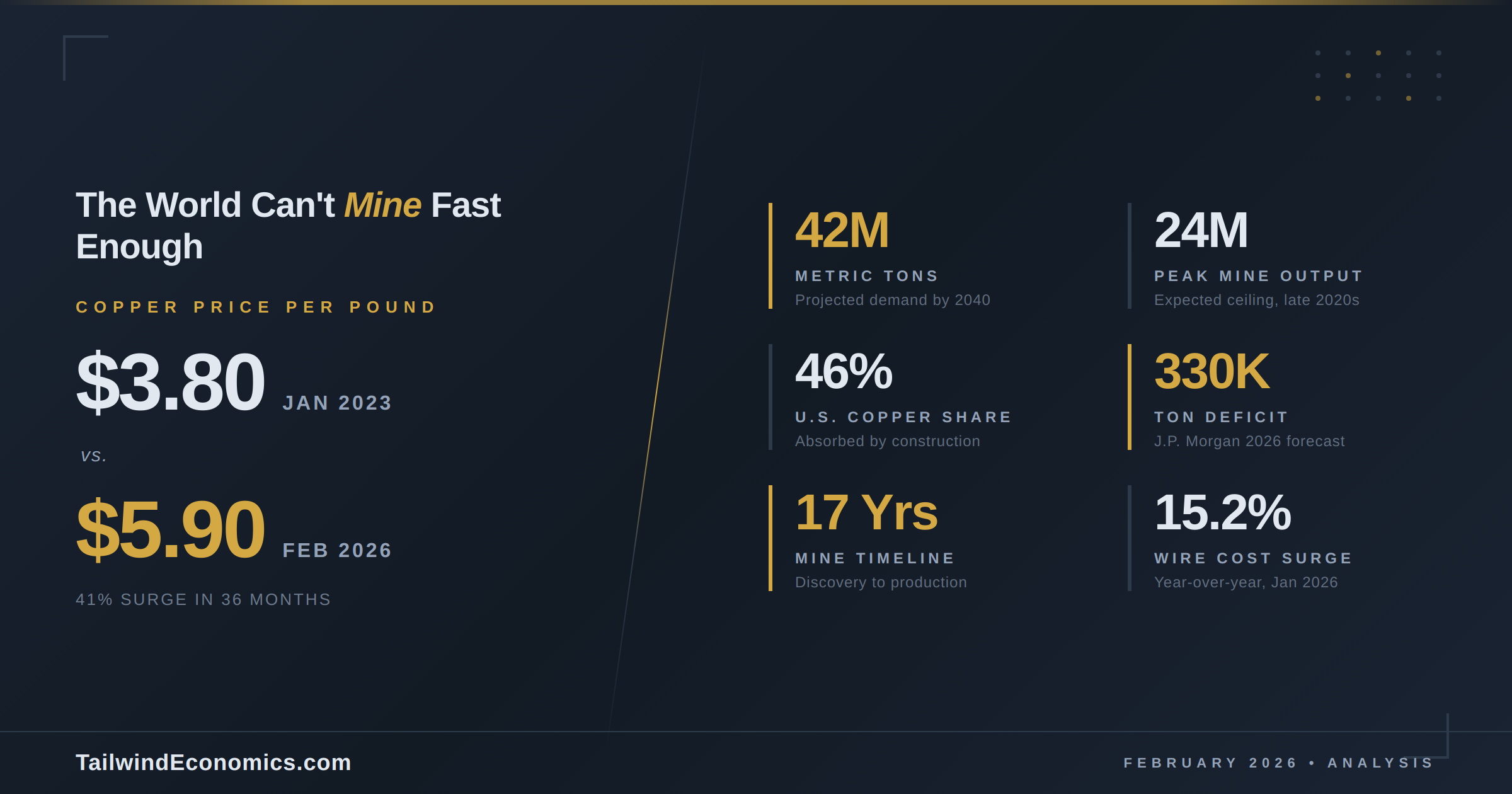

Copper prices have surged to historic levels, and the forces behind the rally suggest this is no ordinary commodity cycle. Trading near $5.90 per pound on COMEX and $12,800 per metric ton on the LME in February 2026, copper has climbed roughly 41% over the past year, breaching $14,500 per metric ton on LME forwards in January before settling into a volatile range. The metal that underpins electrification, construction, and digital infrastructure now sits at the center of a collision between insatiable demand and structurally constrained supply — with profound consequences for industries from homebuilding to artificial intelligence.

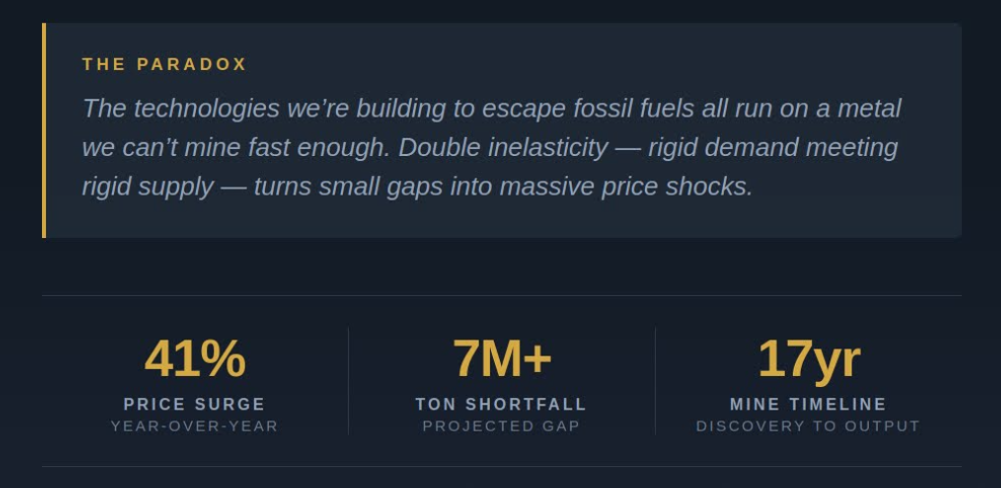

This is not simply a story about a commodity getting more expensive. It is a story about the physical limits of an economic transformation. The world's accelerating push toward electrification, renewable energy, and AI-powered computing demands vastly more copper than the mining industry can deliver on current trajectories. S&P Global projects copper demand will reach 42 million metric tons by 2040 — a 50% increase from today — while mine output is expected to peak near 24 million tons by the late 2020s before declining. The resulting gap, potentially exceeding 7 million tons annually, represents what Daniel Yergin of S&P Global calls an unprecedented challenge: "The world has never produced so much copper in such a short timeframe as would be required."

From $3.80 to nearly $6 in three years

The price trajectory tells a stark story. Copper opened 2023 at roughly $3.80 per pound, drifted to a low of $3.56 by October, then began a relentless ascent. A brief spike to $5.20 in May 2024 — then a record — was followed by a pullback, but the metal closed 2024 near $4.02 before rocketing higher in 2025. On July 24, 2025, COMEX copper hit an intraday all-time high of $5.959 per pound amid fears over a 50% U.S. tariff on copper imports announced under Section 232 authority. A sharp 20% correction followed when refined copper was temporarily exempted, but the fundamental upward pressure reasserted itself. By January 6, 2026, LME cash copper reached $13,387 per metric ton — another record.

The International Copper Study Group now projects a 150,000-ton refined copper deficit in 2026, reversing its earlier forecast of a surplus. J.P. Morgan sees an even wider 330,000-ton shortfall. Bank of America has flagged the potential for spikes to $15,000 per metric ton. Even Goldman Sachs, the most bearish of the major banks with a projected 300,000-ton surplus, raised its 2026 average forecast to $11,400. The divergence among analysts reflects genuine uncertainty — but the direction of prices over three years is unambiguous.

Three forces converging on a single metal

The demand story rests on three pillars, each formidable alone and transformative in combination. First, the energy transition demands copper at an extraordinary scale. An electric vehicle requires roughly 53 to 83 kilograms of copper — up to four times more than a conventional car. Offshore wind turbines consume approximately 5 tonnes per megawatt of capacity, solar installations about 5.5 tonnes. Wood Mackenzie projects EV-related copper demand alone will climb from 1.7 million tons today to 4.3 million tons by 2035. Goldman Sachs estimates that power grid upgrades will drive over 60% of copper demand growth through the decade — "equivalent to adding the copper demand of another United States."

Second, AI and data centers have emerged as an unexpected demand accelerant. A hyperscale AI data center can consume 27 to 33 tonnes of copper per megawatt of installed capacity, more than double a conventional facility. BloombergNEF forecasts data center copper consumption peaking at 572,000 tonnes annually by 2028. Crucially, copper represents less than 0.5% of total data center project costs, making this demand essentially price-inelastic. These facilities will be built whether copper costs $10,000 or $20,000 per ton.

Third, supply simply cannot keep pace. Average copper ore grades have fallen 40% since 1991, meaning miners must process far more rock per unit of metal. New mine discovery rates have plummeted 70% since the 1990s, and the average development timeline from discovery to production now stretches 17 years. The September 2025 catastrophic mud rush at Freeport-McMoRan's Grasberg mine — the world's second-largest — forced a declaration of force majeure that may not be fully resolved until 2027. Chile's Codelco, the state copper giant, hit a 25-year production low in 2023 and is still clawing back output. Meeting projected demand would require opening three world-class mines every year for nearly three decades at a cumulative cost exceeding $500 billion.

Construction feels the pressure first

The construction industry, which absorbs roughly 46% of U.S. copper supply, is absorbing these price increases most directly. Copper electric wire reached $395.15 per thousand linear feet in January 2026, up 15.2% year-over-year according to Gordian RSMeans data. The Producer Price Index for copper and brass mill shapes climbed 11.8% in 2025 alone. Electrical contractors report wire and cable costs rising 40–60% over two years.

While copper typically represents 2–3% of a commercial building's total cost, the proportion climbs sharply in electrical-intensive projects. Data center construction — where electrical systems account for 40–50% of total project budgets — is particularly exposed. With data center construction starts hitting $53.7 billion through November 2025, up 138.6% from the prior year, the compounding effect of rising copper prices on an expanding market is substantial. As Ken Simonson, chief economist of the Associated General Contractors of America, warned in January 2026: "The cost of copper in construction equipment and projects is sure to go even higher this year if the tariffs stay in place."

The automotive sector faces a parallel squeeze. A $1,000-per-ton copper price increase adds approximately $83 to $100 to battery electric vehicle manufacturing costs. Tesla and General Motors have responded by validating aluminum wiring harnesses, trimming 10–15 kilograms of copper per vehicle, while 800-volt architectures in newer EVs reduce cable thickness and associated copper content.

Hedging against the new reality

For firms dependent on copper, the question has shifted from whether prices will stay elevated to how to manage the exposure. COMEX copper futures — standard contracts of 25,000 pounds — remain the primary hedging instrument, allowing manufacturers and contractors to lock in forward prices. Collar strategies, combining purchased put options with sold calls, offer bounded protection without large upfront premiums. MetalMiner and other procurement advisors recommend pairing modest physical buffer stocks with active financial hedges.

On the contractual side, escalation clauses have moved from optional to essential. ConsensusDocs 200.1 is the only standard construction form offering a dedicated price escalation provision. Increasingly, firms negotiate threshold-based escalation — triggering compensation only when copper exceeds a defined percentage above the bid price — with symmetric de-escalation for price declines. Firms that secured long-term fixed-price supply agreements in 2024 and early 2025 are now operating with significant cost advantages over competitors reliant on spot markets.

A supercycle or a speculative peak?

The debate over whether copper has entered a genuine commodity supercycle — a multi-year period of prices sustained well above historical trend — remains unresolved. Bulls point to structural supply deficits, the IEA's projection of a 30% supply shortfall by 2035, and the unprecedented simultaneous pull from electrification, AI, and defense. Veteran investor John Polomny now uses the word without hesitation: "Supercycle."

Bears counter with legitimate concerns. Goldman Sachs notes that 2025 produced a 600,000-ton surplus, the largest since 2009, even as prices hit records — suggesting financial speculation and tariff-driven U.S. stockpiling (over 515,000 tons in COMEX warehouses) are distorting fundamentals. Chinese refined copper demand fell an estimated 8% year-over-year in Q4 2025. The copper-to-aluminum price ratio has crossed 3.7:1, surpassing the 3.5:1 threshold that historically triggers industrial substitution. Wood Mackenzie's Julian Kettle offers a pointed reminder: "Too many forecasts ignore that aluminum is a serious competitor. Excessively high prices for copper will not be good for the metal in the long term."

The economic theory cuts both ways. Copper demand and supply are both highly inelastic in the short run — an IMF study found that a 10% demand-driven price shock increases same-year output by only 3.5%. This double inelasticity explains why small imbalances produce outsized price swings. But it also means that sustained high prices will eventually activate substitution, scrap recovery (already 30–35% of U.S. supply), and new investment — the self-correcting mechanism that has historically prevented permanent scarcity.

What the price of copper is really telling us

The most honest reading of the copper market is that it is pricing in a real and daunting physical challenge while simultaneously reflecting short-term distortions — tariff arbitrage, speculative positioning, and Chinese policy shifts — that inflate volatility beyond what fundamentals alone would dictate. The structural story is sound: the world needs dramatically more copper than it currently produces, the timeline to develop new supply is measured in decades, and the applications driving demand growth are non-discretionary pillars of economic policy worldwide. But the path from here will not be a straight line upward. Demand destruction, aluminum substitution, and the eventual resolution of the U.S. tariff regime will create corrections that test conviction. For the industries that depend on copper — construction, automotive, energy, telecommunications — the imperative is clear: treat elevated prices not as a temporary disruption but as a structural feature of the economic landscape, and build procurement, hedging, and design strategies accordingly.